简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Full force of central banks siphoning world liquidity: Mike Dolan

Abstract:Coordinated or not ahead of this month’s G7 summit, global central banks are accelerating interest rate hikes but also actively draining the giant pool of cash swilling around world markets and buoying currencies to stymie imported inflation.

You dont have to be a strict monetarist or liquidity obsessive to see how the scale of this will affect stocks and bonds over the remainder of the year at least.

For many who do focus on the lockstep impact of world liquidity on asset prices, the process has already been underway since late last year and has been the driver of the 20-30% drop in major stock indices since December.

The worrying bit for investors is that it may only be about half-way through and the aggressive tightening unveiled this week shows little trepidation among policymakers right now.

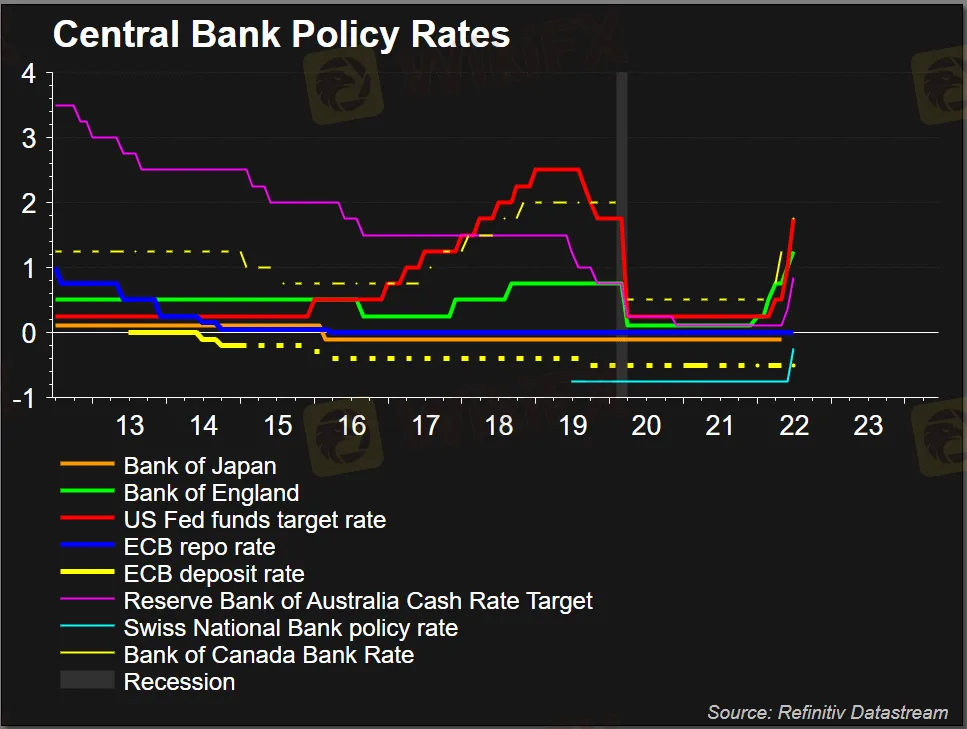

This weeks headline grabbing interest rate rises from the U.S. Federal Reserve, Bank of England and Swiss National Bank show new-found determination to get across decades high inflation as quickly as possible while unemployment rates are near historic lows and labour markets remain tight.

The European Central Bank grappled with how to rein in ballooning euro sovereign risk premia as it prepares to raise rates next month for the first in more than a decade. But agreement on the “anti-fragmentation” backstop was seen as a quid pro quo for steeper policy rate rises and markets now price almost 2 percentage points of hikes by the year-end.

The Feds outsize 75 basis point rate rise was its biggest move in 28 years, with markets now expecting its key rate to more than double from new target range of 1.50-1.75% within a year. Even grappling with a much weaker economy, the Bank of England is also expect to almost double rates to more than 2% from here.

The shock half-point rise in SNB rates on Thursday threw another log on the fire, leaving a lonely Bank of Japan the only one of the major players still pegging short and long-term borrowing rates down.

Technical recessions may now be an inevitable price to pay. Some argue that allowing inflation to stay so high may trigger one anyway by squeezing real incomes and company margins hard.

But higher central bank borrowing rates are just one part of the story and the great unwind of central bank balance sheets is arguably a far more direct impact on world markets.

Secretly draining

According to liquidity specialists CrossBorderCapital, the annual percentage change in central bank liquidity has already collapsed and is contracting from peak annual expansion rates of about 40% last year.

In note published just before this week‘s barrage of official rate rises, it stressed that this contraction was underway before this month’s start of the Fed‘s “quantitative tightening” (QT) or next month’s ECB equivalent – however messy the latter may be in the light of a new “fragmentation” buster.

And it expected an annual contraction of up to 10% to persist for the next two years.

The Feds contribution to the fabled punchbowl this year is a case in point.

Even though its overall balance sheet brims at well over $8 trillion on the eve of QT, commercial bank reserves held at the Fed – a flipside of balance sheet assets and where the real liquidity to world markets comes from – have dropped by almost $1 trillion since December as U.S. Treasurys account at the Fed refilled.

And thats before some $1-$2 trillion of overall balance sheet reduction comes down the pike over the next 18 months.

Claiming the Fed has been “secretly shrinking liquidity injections” this year, CrossBorderCapital sketches how the confluence of reduced Treasury bill sales and rising Fed rates draws more and more of that money into Fed reverse repurchase operations – currently running at more than $2 trillion nightly.

That further shrinks the “effective Fed balance sheet” and that could now halve by 2025 due the combination of outright balance sheet decline and the draw of reverse repos.

“A rising tide may well float many boats, but a tsunami of monetary tightening unquestionably sinks asset markets,” it concludes.

While this may appear like arcane accounting, the shift in these liquidity measures tallies uncannily with market pricing.

Beyond the Fed, the ECB picture may seem messier. But BoE balance sheet reduction is also due and the SNBs surprise rate hike rates sees it embrace a strong Swiss franc to dampen imported inflation and likely stop its FX-related balance sheet accumulation of global stocks and bonds.

Whats more, the aggressive turn in Fed tightening promises even more dollar strength ahead, forcing other central banks into similar tightening for fear of exaggerating their inflation pictures with ever higher dollar-based energy and food imports as well as tightening borrowing conditions for emerging markets.

“The last decade was a race to the bottom in currency wars globally, with lacklustre inflation dynamics, but the mood music has now changed,” said Charles Hepworth, Investment Director at GAM Investments.

The author is editor-at-large for finance and markets at Reuters News. Any views expressed here are his own

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

U.S. Stocks Bounce Back for Two Consecutive Days, Is a Positive Outlook Ahead?

The U.S. stock market has rebounded for two consecutive days. Could this signal a potential turning point, or is it just a temporary uptick? Let's explore the market movements, their underlying causes, and how investors should respond.

U.S. Consumer Weakness: Is It Good or Bad?

U.S. retail data for February came in below expectations, raising concerns about slowing consumer spending. Does this signal the beginning of an economic slowdown, or is it just a temporary fluctuation? Let's dive into the analysis.

Acuity Trading and interop.io have joined forces

Acuity Trading and interop.io have joined forces to streamline financial data integration, enabling traders, brokers, and institutions to access real-time market intelligence without disrupting their existing systems. This partnership represents a significant step forward in addressing one of the financial industry’s most persistent challenges—integrating vast amounts of market data from diverse sources.

How to Avoid Risks from Scam Brokers in Forex Investment?

In recent years, the forex market has become a popular choice for global investors due to its high liquidity and 24-hour trading advantages. However, according to the recently concluded WikiFX "3·15 Forex Rights Protection Day " event, we received over 6,000 pieces of evidence exposing rights violations within a short period. This reflects that, although the forex industry is becoming more regulated, fraudulent platforms continue to emerge, causing significant suffering for many victims.

WikiFX Broker

Latest News

Beware: Forex Investment Fraud Targeting Low Income Earners

WikiFX

WikiFXCentral Bank Policies,Forex Markets and Gold Prices

WikiFXThese 24 Crypto Scams Are Accelerating the Theft of Your Assets

WikiFXBeware of Fake 'Educational Foundations' Targeting Crypto Investors, Warns North Dakota Regulator

WikiFX49 Foreigners Arrested in Illegal POGO Raid in Pasay City

WikiFXWe Asked Grok About Illegal FX Brokers—Here’s What It Revealed

WikiFXExposing Trading Academy Scams: How Aspiring Traders are at Risk

WikiFXOnline Investment Scams on the Rise: How Two Victims Lost Over RM100K

WikiFXVanished Savings: How One Woman Lost RM412,443 to an Online Scam

WikiFXInvestor Alert: FCA Exposes 9 Unregistered Financial Companies

WikiFXCurrency Calculator